'It's going to hit the consumer hard': Those with higher credit scores may pay higher mortgage fees

BOSTON - Changes in the mortgage industry could spell bad news even if you have good credit.

Beginning May 1, some people with higher credit scores may actually end up paying a higher fee while those with lower scores will pay less.

"It's really a big change," explained mortgage loan officer and credit score expert Al Bingham. "It's going to hit the consumer hard when they go to apply for a mortgage."

What is changing on May 1?

The Federal Housing Finance Agency (FHFA) is recalibrating the fee structure for loan-level price adjustment (LLPA) by lowering fees for some borrowers and hiking those for others.

"The spread of fees between low and high credit score borrowers won't be as big," Zillow economist Orphe Divounguy told CBS MoneyWatch.

For instance, starting in May a homebuyer with a credit score between 640 to 659 - considered "fair" - and who has a down payment of 5% will incur an LLPA of 1.5%. Prior to the change, the fee for this group of buyers was 2.75%. That means someone purchasing a $200,000 home would pay an LLPA fee of $3,000 under the new structure, down from $5,000 previously.

But some purchasers won't get as good deal as they did before. For instance, homebuyers with credit scores of 740 to 759 - considered "very good" - and putting 20% down will face a new LLPA of 1%, compared with 0.5% previously. For the purchase of a $200,000 home, that means the fee will double to $2,000.

The changes are part of the federal government's effort to provide equitable access to home ownership.

According to Bingham, it comes down to fees that lenders pay back to federal programs that back the mortgages. For some first-time homebuyers, those fees are often rolled into a higher interest rate paid by the consumer.

Here is what it will mean for first-time homebuyers who fit certain income guidelines.

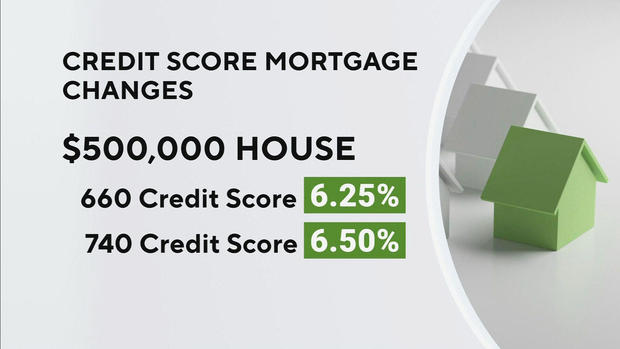

For a homeowner with a $500,000 purchase price who puts down the minimum down payment, a person with a 660 credit score will get a rate of about 6.25% while a buyer with a 740 score will pay 6.5%.

The changes will also make it more expensive for borrowers to refinance and to pull equity out of their homes to pay off consumer debt.

So, should you lower your credit score to get a cheaper fee? No.

One media report cited an unnamed expert advising people to lower their credit scores to get a better fee, but that's terrible financial advice, experts say.

First off, people with higher credit scores are still paying lower fees, so it doesn't make sense to damage your credit score. Second, that can ruin your prospects of getting better rates for other loans, such as auto loans or credit card rates.

"The bottom line is if you have a higher credit score, you will pay less than someone with allow credit score," Divounguy said.

According to the Federal Housing Finance Agency, while some fees are being eliminated for lower-income buyers, and fees are being increased for for some buyers with higher credit scores, the two are not cause-and effect. "Higher-credit-score borrowers are not being charged more so that lower-credit-score borrowers can pay less," they said in a statement. "Some updated fees are higher and some are lower, in differing amounts. They do not represent pure decreases for high-risk borrowers or pure increases for low-risk borrowers." You can read their full explanation of the fee changes on their website.