Uh oh -- just 8 stocks are propping up the market

Despite a rip-roaring rally in October, all is not well on Wall Street. With the Dow Jones industrials stalled just below the 18,000 level, hopes for a "Santa Claus rally" to end the year have dimmed.

In fact, an analysis by Goldman Sachs found that if not for a group of just eight stocks -- dubbed the "FANG" and the "NOSH" stocks -- the S&P 500 would actually be in negative territory for the year to date. The FANGs are Facebook (FB), Amazon (AMZN), Netflix (NFLX) and Alphabet (GOOGL). The NOSHs are Nike (NKE), O'Reilly (ORLY), Starbucks (SBUX) and Home Depot (HD).

This is a consequence of growing fear and uncertainty that an interest rate hike from the Federal Reserve at its December policy meeting won't be as benign as the optimists hope. As a result, investors aren't only shying away from a growing number of stocks but also from assets in other markets such as commodities and high-yields bonds.

To cut to the quick: The specter of the first increase in the cost of credit since 2006 is set to further strengthen the U.S. dollar, which is on the verge of returning to highs not seen since early 2003. That could set off a nasty cascade effect.

A stronger dollar would likely pressure corporate profit margins by weighing on commodity prices and reducing the value of foreign earnings. Both were highlighted as drags during the recent third-quarter earnings reporting season, which is on track to result in the first back-to-back earnings decline since the recession ended. Revenues are heading for the third consecutive quarter of declines.

A rate hike would then threaten debt-funded corporate share repurchase programs that have played such a big role in bolstering earnings-per-share metrics and supporting stock prices during this bull market. This is driven by a combination of higher bond yields, widening credit spreads (the difference in yield between corporate bonds and U.S. Treasury bonds, a measure of risk) and subdued earnings growth.

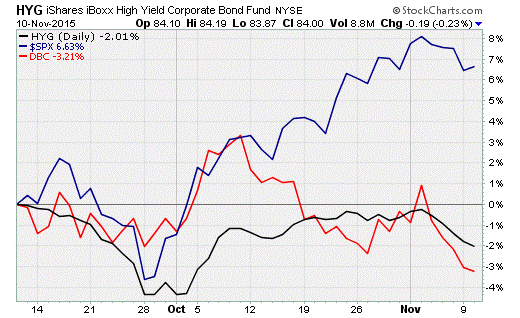

Thanks to the strength of the FANGs and the NOSHs, the S&P 500 (blue line above) has separated from growing weakness in high-yield corporate bonds (black line) and commodity prices (red line). I don't think equities can continue to stand alone much longer based on the performance of a small group of big-tech and consumer stocks.

For one, they're expensive. On a price-to-earnings ratio, Amazon is trading at 900 times earnings. Netflix is trading at 292 times earnings. Facebook is trading at 107 times earnings. The overall S&P 500 is trading at 20 times earnings, above its long-term average.

Here's the crux of the problem.

Debt-funded repurchases have been a big deal. According to data from Standard & Poor's, S&P 500 companies have purchased $2.5 trillion of their own stock between first-quarter 2009 and second-quarter 2015. These purchases boost earnings when financing costs are below the forward earnings yield of the shares purchased.

A Fed rates liftoff and the consequences that will follow -- strong dollar, weak commodities and higher long-term yields -- could quickly flip this dynamic and starting in 2016 remove one of the biggest single sources of buying demand from the stock market.

An analysis by Yardeni Research shows that, excluding financials, the S&P 500 outstanding share count has fallen nearly 8 percent since 2005, led by a 17.9 percent drop for consumer discretionary stocks and a 16.1 percent tumble in tech stocks.

Stocks in these areas, including the FANGs and the NOSHs, would be hardest hit by any weakness connected to a slowdown in buyback programs resulting from the fallout of the Fed's policy tightening.

Without these eight stocks providing support, the next big move in the market could see the major equity averages return to their August-September lows rather than triumphantly blast to new record highs, which seemed so likely just a few weeks ago.