The dangers of dividend-paying stocks

The current low-interest-rate environment has caused many investors to search for sources of incremental yield. Two of the more popular approaches involve dividends: stocks with high dividends (or higher yields than available from safe fixed income investments) and stocks with fast-growing dividends. We will examine two of these alternatives to see if they're good choices.

High-dividend stocks

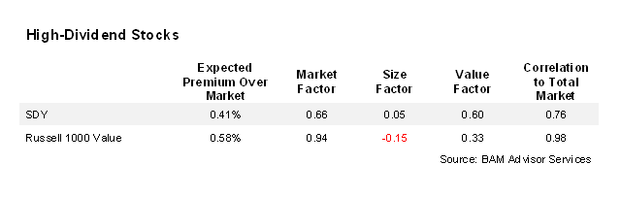

To represent high-dividend stocks, we'll use the SPDR S&P Dividend ETF (SDY). This ETF tries to match the total return performance of a dividend-stock index, the S&P High Yield Dividend Aristocrats Index.

While the current dividend yield of the S&P 500 Index is about 2 percent, the yield on SDY is about 3.2 percent. So, that's the attraction, but is it the best way to achieve the goal? We'll analyze the fund using a three-factor regression, which means analyzing the fund's exposure to three major risk factors:

- Beta -- or the exposure to stock-market risks

- Size -- or the risk of small-cap stocks

- Value -- or the risk of value stocks

We find that SDY is really a less-diversified, large-cap value strategy, holding just 61 128 stocks. You can see the value orientation in the table below (which covers the period May 2006 [fund inception] to December 2011) -- the fund has a high "loading" of 0.6 on the value factor, meaning it has more exposure (almost twice) to the value factor than does the Russell 1000 Value Index.

The fund's high exposure (0.66) to market risk and (when compared with the Russell 1000 Value Index) value risk, clearly shows that an investment in SDY isn't much more than a value-oriented equity strategy. For those seeking exposure to the value factor there are more efficient ways to accomplish this objective.

Fast-growing dividend strategy

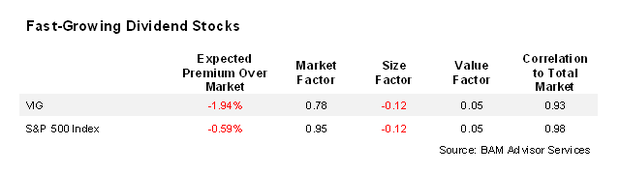

To represent fast-growing-dividend stocks, we'll use the Vanguard Dividend Appreciation ETF (VIG). This ETF seeks to track the performance of the Dividend Achievers Select Index, which consists of common stocks of companies that have a record of increasing dividends over time. The current dividend yield is about 2.1 percent. When looking closer at this fund, we find that VIG looks like a less diversified S&P 500 fund, holding just 144 61 stocks. The fund has the exact same exposure to the size and value factors as does the S&P 500 Index, although it has a lower exposure to beta, or market, risk.

Why these aren't good substitute strategies

In both cases, the funds had significant exposure to market risk, which makes total sense since they're both baskets of stocks. This means they have entirely different risks than bonds, which are meant to be safe havens during difficult market periods.

4 things every bond investor should know

Although the dividends from these two strategies may provide higher yields than bonds in this current environment, keep in mind what would likely happen if the market heads south again. Not only would the value of the stocks drop, but the companies may choose to trim or even eliminate their dividends. Certainly, that's what we saw in 2008, as SDY's net asset value dropped 23 percent and VIG's NAV fell 26 percent.

At least you now have the facts, and hopefully a better understanding of the nature of these strategies and the risks they entail. Informed investors generally make better decisions.

Image courtesy of www.lumaxart.com.