Tax strategy may affect Medicare premiums

(MoneyWatch) When I wrote about how you should plan for the fiscal cliff, I noted that you might want to consider accelerating income into 2012. Next year, we'll see the 3.8 percent Medicare tax, plus a possible increase in tax rates for capital gains, while for those at higher income levels ordinary income tax rates are almost certain to rise as well.

My Buckingham Asset Management colleague Jim Cornfeld noted that this strategy may have some negative implications for people over 65 who are receiving Medicare benefits, implications that should be considered. I thank Jim for sharing his thoughts below.

Under the Medicare law, if you have a high-enough income, you have to pay extra for Part B and prescription drug coverage. The amount depends on your modified adjusted gross income (MAGI), which is your adjusted gross income plus tax-exempt income. These increases are based on your MAGI from two years prior, meaning your 2012 MAGI may affect your 2014 premiums.

- Tax tips: How to realize gains early

- Pending tax changes affect portfolio management

- How investors should plan for the "fiscal cliff"

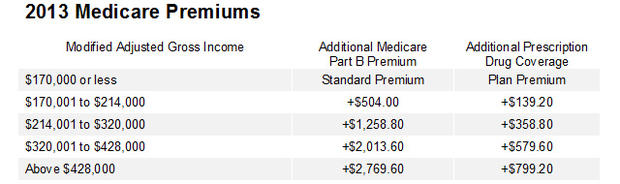

Below is the table showing increases in 2013 Medicare premiums based on 2011 MAGI. (Please note that the information is for married couples filing jointly. The information for individuals and married couples filing separately can be found on the Medicare website.)

This example illustrates how taking additional income this year in light of next year's tax increases can affect Medicare premiums. Let's say you and your spouse have MAGI of $150,000 and qualify for the standard premium. You're also guessing that capital gains rates will rise by 5 percent, so you want to realize $300,000 this year, saving $15,000.

However, the extra capital gains income means your MAGI goes up to $450,000, increasing your Medicare premiums by $3,568.80 ($2,769.60 + $799.20, assuming the rates remain the same). Keep in mind that this increase is per person. If both you and your spouse take Medicare benefits, your premiums will increase by a total of $7,137.60, or about half the amount you planned to save by realizing gains this year.

Now, what if you want to realize much larger gains, say, $1 million? If you're still guessing at a 5 percent increase in the capital gains rates, you're looking at $50,000 in savings, while the extra Medicare cost is still $7,137.60, or about 14 percent of the expected tax savings. Obviously, this isn't as large, but still something to be aware of.

Finally, this will only have a one-year impact. If MAGI falls back to the previous level, then Medicare premiums will also fall back to the standard. Of course, it's important to remember that you should always consult your tax advisor prior to implementing any tax strategies.