Stock market bulls are running into reality

A number of catalysts were in play on Thursday that hit U.S. equities hard, with the major indexes on the cusp of breaking their seven-week-plus uptrends.

For one, normally dovish Chicago Fed President Charles Evans raised expectations of two rate hikes this year (vs. market expectations for just one). Regulatory worries remain acute as the White House clamps down on corporate tax inversions, dampening M&A activity.

Plus, overseas European bank stocks were under pressure on fears over European Central Bank rates cuts deeper into negative territory. And Japan was suffering as Prime Minister Abe and the Bank of Japan look increasingly toothless to reinvigorate the Japanese economy.

All of this is bad news for financial stocks, which suffered some big breakdowns. Negative interest rates pinch banks' net interest margins (the difference between their cost of money and the interest rate they lend at) and in particular put further pressure on already vulnerable eurozone banks. A more aggressive Fed rate hike schedule threatens to destabilize global markets and rattle currency valuations.

Stocks in the banking sector lost 1.9 percent to lead Thursday's decliners.

After seven weeks in which the bulls pretty much had it all their own way -- capped by last week's super-dovish speech by Fed Chair Janet Yellen -- investors are coming back to reality as the start of the first-quarter earnings season looms on April 11 when Aloca (AA) reports.

Analysts are looking for S&P 500 earnings to decline 8.5 percent over last year's first quarter -- on track for the fourth consecutive period of falling profitability. Corporate profits peaked in the second quarter of 2015. Recessions typical start five to seven quarters afterwards.

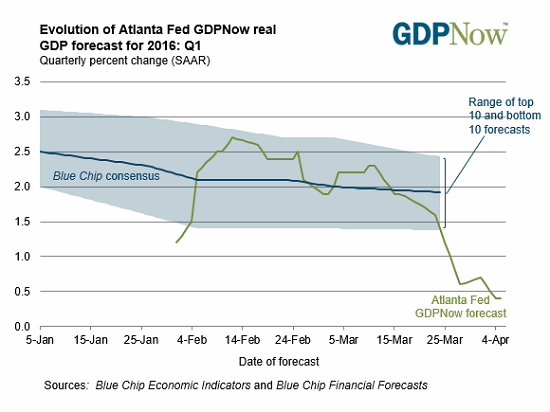

The current U.S. economic expansion is looking old and feeble. The Atlanta Fed's GDPNow tracking estimate of first-quarter growth recently got cut to just 0.4 percent (chart above), and Fed policymakers admit that despite strong job gains, they don't feel confident enough yet to raise rates again. Factory activity remains tepid, with new orders and shipments on the decline since late 2014.

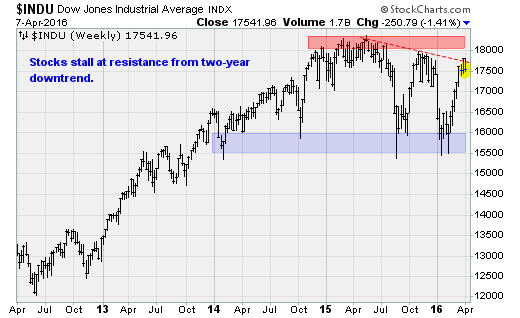

The technical and fundamental outlook still looks challenging for stocks as the Dow Jones industrials contend with major overhead resistance near the 18,000 level (chart above).

The price-to-sales ratio of U.S. stocks hasn't been higher since the subprime bubble blew. Debt-funded corporate stock buybacks -- a major source of buying demand for equities -- look vulnerable as buybacks as a percentage of operating income has reached a record high. Net debt-to-equity ratios have jumped out of their historic range as balance sheet leverage amps up.

Strategists from JP Morgan warned clients this week to brace for the end of the seven-year bull market: "This is not the stage of the U.S. cycle when one should be buying stocks with a six- to 12-month horizon. We recommend using any strength as a selling opportunity."