Time to revisit Roth vs. traditional IRA and 401(k)

Here's another financial matter to consider now that the U.S. has a new tax law: Do you know which is better for you -- a Roth IRA or Roth 401(k) account, or a traditional IRA or traditional 401(k) account? As with many tax issues, there's no pat answer that applies to everybody. Rather, the answer falls into the "it depends" category.

That's because many rules and nuances for either type of account might apply to your situation, and one prime consideration is the new marginal tax rates that will apply starting in 2018.

To determine which type of IRA or 401(k) might work best for your situation, let's first review the key differences between the two types of accounts.

A brief review of the rules

With a traditional IRA or 401(k) account, you reduce your current taxable income by the amount of your contribution, and you aren't taxed on your investment earnings while your savings grow. Years later, when you withdraw money from your savings during retirement, the amount of your withdrawal is counted as taxable income.

With a Roth IRA or 401(k) account, it's the other way around: You don't get a tax deduction for the amount of your contribution, but you also won't have to pay income tax on your contribution when you withdraw the money after you retire. Like a traditional IRA or 401(k) account, your investment earnings aren't taxed while your money grows.

However, unlike a traditional IRA or 401(k) account, you'll pay no taxes on your investment earnings at all if you've had your Roth IRA or 401(k) account for at least five years and withdraw your investment earnings after attaining age 59-1/2 (note that certain exceptions apply).

Because of these key differences, one of the most important factors to consider when comparing the two types of IRAs and 401(k) accounts is whether you expect your current marginal income tax rate to be higher or lower than the marginal income tax rate that will apply after you retire and make withdrawals. The common argument for using a traditional IRA or 401(k) account is based on the assumption that you'll be in a lower tax bracket when you retire.

Note that if your current and future marginal tax brackets are equal, there's no difference mathematically between the two types of accounts in the amount of aftertax income you'll receive in retirement. In that case, the tax considerations shouldn't be a deciding factor for you.

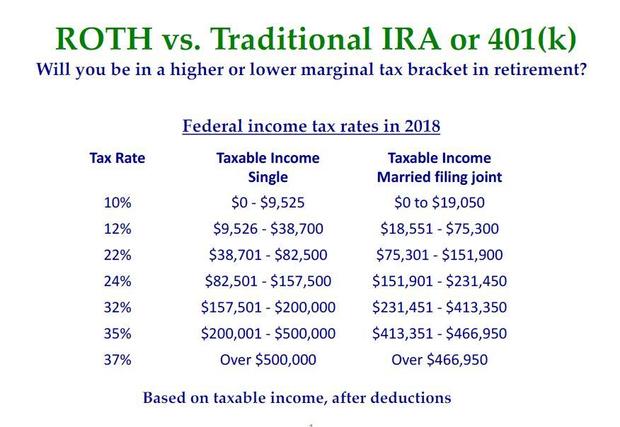

The new tax rates

The table below shows the new marginal tax rates in 2018 for single workers or married couples filing jointly.

Don't forget that the taxable income amounts are determined by deducting the standard deduction amounts, which have increased under the new law as follows:

- Single: $12,000

- Married filing jointly: $24,000

If you're age 65 or older, blind, or disabled, you can add $2,600 to your standard deduction if you're married and both spouses are over age 65, and $1,600 if you're single.

So how do you know if you'll be in a lower tax bracket when you retire compared to when you were working? It depends significantly on your taxable income before and after retirement.

One thing to keep in mind is that depending on the amount of your income from all sources, part or all of your Social Security income will be excluded from your taxable income. For the highest earners, at least 15 percent of your Social Security benefits will be excluded. As a result, many people will experience a significant drop in their taxable income in retirement, particularly if they have no significant pension from their employers and if their retirement savings are modest (which describes millions of older workers).

Examples illustrate the possibilities

Let's look at a few examples to see how the new tax rates might influence your decision to use Roth or traditional contributions.

- Suppose you're working and currently paying taxes at the 12 percent marginal rate. This applies to single workers with taxable income between $9,526 and $38,700 ($18,551 to $75,300 for married filing jointly). The top ends of these ranges translate to gross incomes of $50,700 or $99,300, respectively, when you add the standard deduction for workers under age 65 to the taxable income amounts. In this situation, there's a good chance you'll be paying taxes at a 10 percent rate in retirement, not much of a drop from when you were working. As a result, there's not much advantage to using a traditional IRA because your marginal tax rate wouldn't drop very much.

- Suppose you're working and currently paying taxes at the 22 percent marginal rate. This applies to single workers with taxable income between $38,701 and $82,500 ($75,301 to $151,900 for married filing jointly). In this situation, there's a good chance you'll be paying taxes at a 12 percent rate in retirement or lower, resulting in at least a 10 percent drop compared to when you were working. In this case, it would be advantageous to use a traditional IRA.

- Suppose you're working and paying taxes at the 24 percent marginal rate. This applies to single workers under age 65 with taxable income between $82,501 and $157,500 ($151,901 to $234,350 for married filing jointly). In this case, if you experience a modest reduction in income when you're retired, you might be paying taxes at a 22 percent marginal rate, not much of a drop and not much of an incentive to use a traditional IRA. On the other hand, if you experience a significant drop in income in retirement, you might be paying taxes at a 12 percent or even 10 percent rate. In this case, it would be advantageous to contribute to a traditional IRA.

The logic that applies to workers in the 22 percent and 24 percent marginal tax brackets might also apply to workers currently paying taxes at the 32 percent and 35 percent brackets.

Consider the Required Minimum Distribution

Roth IRAs aren't subject to the required minimum distribution (RMD) at age 70-1/2. Thus, if there isn't much of a tax savings for a traditional IRA or 401(k), you might consider using a Roth IRA or 401(k), which will give you more flexibility when you reach age 70-1/2. Note that Roth 401(k) accounts are subject to the RMD, but not if you roll your Roth 401(k) account to a Roth IRA.

In spite of all these considerations, some people might think the new tax rates are as low as they'll get and that they could increase under a future Congress. This could happen if the federal deficit increases rapidly or if Congress allows the new tax rates to expire after 2025, as the law now stipulates. This belief would make a good argument for contributing now to a Roth IRA or 401(k) account.

If you're still confused or don't know what your marginal income tax rates will be when you retire, consider a form of tax diversification: Split your contributions between the two types of IRAs or 401(k) accounts.

Whatever you do, don't let these rules deter you from making any contribution to an IRA or 401(k) account. No matter what choice you make, you'll be better off saving money for your future than spending it all today.