Maybe consumers won't be boosting the economy

U.S. equities were hit hard on Wednesday as concerns about the retail sector -- ahead of a string of earnings reports from the group -- cast doubt over the American consumer and the vitality of U.S. economic growth.

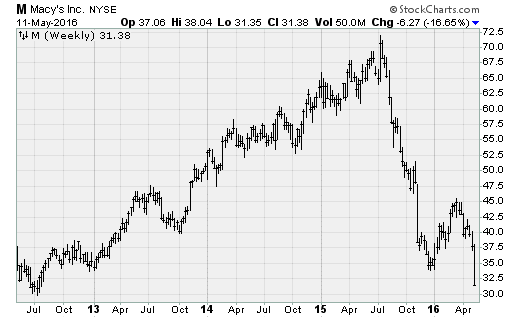

Macy's (M) shares lost 15 percent, closing on Wednesday at $31.38 after reporting more than a 7 percent drop in sales -- a fifth consecutive quarterly slide. The giant retailer also lowered its forward guidance. Earnings came in at 40 cents (vs. 36 cents expected), while sales totaled $5.77 billion (vs. $5.95 billion expected). Sales at stores open a year or more dropped 5.6 percent.

The stock dropped all the way back to its 2012 levels and is now down more than 56 percent from last summer's highs. Ouch.

Management highlighted that weakness in consumer spending worsened in the middle of March -- which was about a month into the epic 50 percent rebound in wholesale gasoline prices -- and it ominously warned that "we are not alone" in the suffering.

The data backs this up: The latest personal income and spending report shows that income growth is strong but spending isn't. In fact, durable goods spending dropped 0.6 percent in March over February.

The weakness in Macy's shares spilled over to other retailers.

Gap (GPS) lost 3.7 percent on weaker comp-store sales. Fossil (FOSL) lost 29.1 percent on weaker-than-expected first-quarter earnings and a 20 percent cut to 2016 guidance on slower spending from tourists and slower watch sales. And Ross Stores (ROST) lost 5.4 percent after being downgraded by analysts at Piper on valuation and weakening consumer spending as interest in off-price stores wanes.

Office Depot (ODP) cratered 40.4 percent, while Staples (SPLS) lost 18.3 percent after the government torpedoed their merger plans on antitrust concerns.

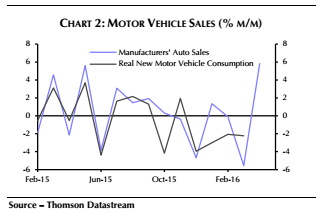

Investors will also be closely watching Friday's retail sales report. The consensus is for a big 0.9 percent month-over-month rise, which would be the best one-month result since early 2015. These hopes are pinned on predictions of robust auto sales and higher prices at gasoline stations.

Yet Deutsche Bank's normally optimistic Joseph LaVorgna warned that his top economic indicators suggest the expected second-quarter bounce back in the economy isn't really materializing. Only low initial weekly jobless claims (which showed an alarming reversal on Thursday) and motor vehicle sales are showing strength. Other signs, including tax receipts, suggest ongoing weakness.

Capital Economics remains sanguine, pointing to the rapid snapback in auto sales in April to a 17.4 million seasonally adjusted annualized rate. This should, in the firm's estimation, boost real consumption growth to a 2.5 percent annualized rate for the second quarter.

For now at least, stock investors aren't buying the sunny outlook as buyers keep their shopping carts bare.