Climate change is making home insurance costs more expensive. These maps show prices and weather risks in your state.

Hurricane Francine in Louisiana, flooding in the Carolinas and wildfires in California are among the extreme weather events impacting millions across the U.S. just in the past week. And it's not just about the physical risks — it's having a major impact on the affordability of having a home, as extreme weather continues to feed into the rising costs of home insurance.

In some areas, homes are such great a risk that they're too expensive to insure — if private insurance is even available at all.

How much does the average person spend on home insurance?

Home insurance premiums are intended to be cheaper than what it would cost to rebuild your home after a disaster or major damage. That cost is based on numerous factors, including home size and claim history, but it's also based on location — and as extreme weather events driven by climate change bring a greater risk of floods, severe storms, hurricanes and heat waves, among other things, that location matters more than ever.

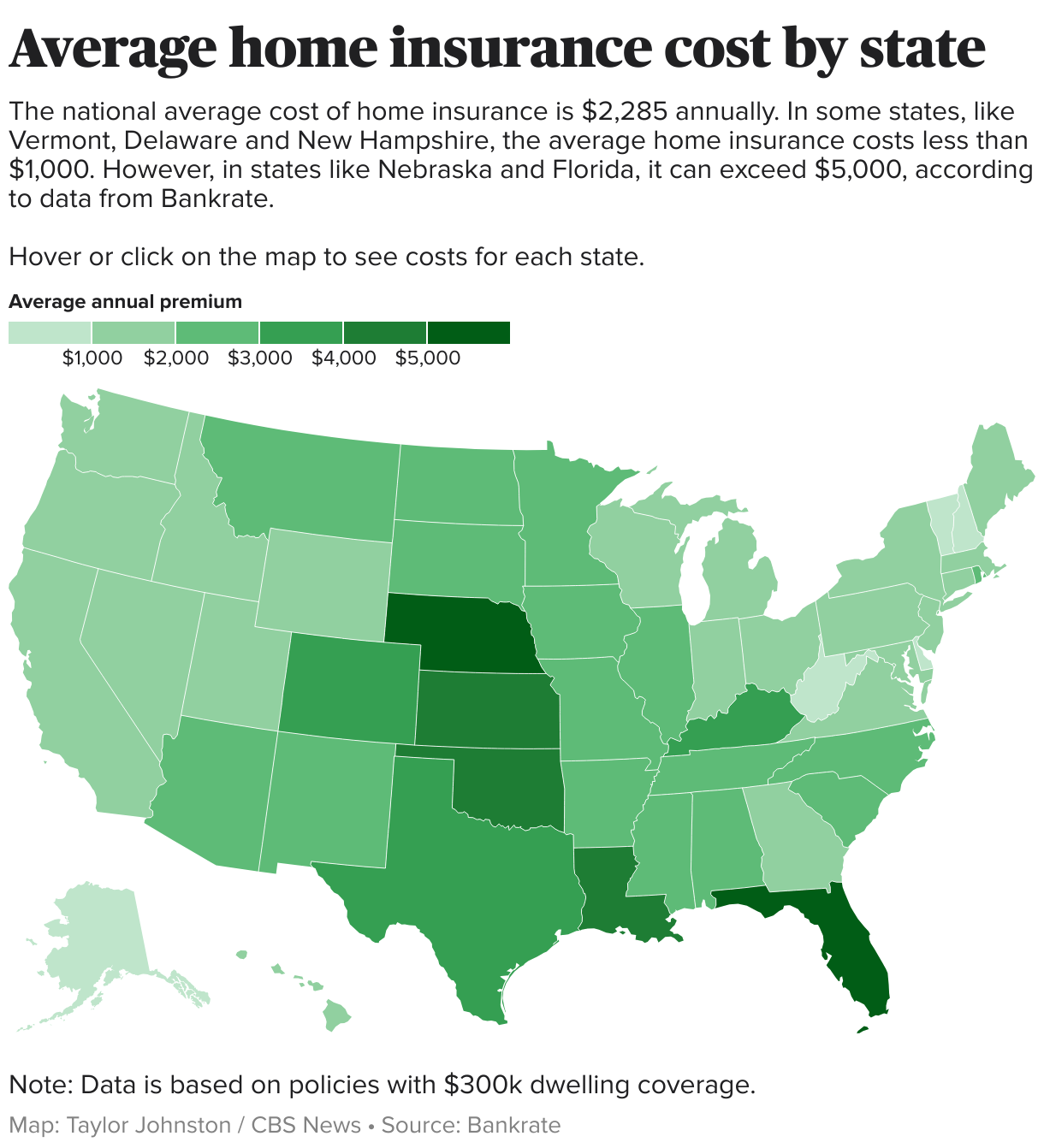

Bankrate has found that the average cost of dwelling insurance, which covers the actual structure of your home should it need to be rebuilt, is $2,285 per year in the U.S. for a policy with a $300,000 limit. But that cost is still rising.

"From 2017 to 2022, homeowners insurance premiums rose 40% faster than inflation," a June report by the Bipartisan Policy Center says. "...For millions of households already struggling to make their mortgage payments, these monthly insurance costs are a significant burden. They can also put homeownership out of reach for prospective first-time homebuyers."

The range of homeowners' insurance costs is widespread. In Vermont, Bankrate data shows that people pay an average of $67 a month for a $300,000 dwelling limit, while in Nebraska, the most expensive home insurance state, people pay an average of $471 per month — an annual policy that amounts to more than $3,300 above the national average.

Other parts of insurance coverage are not included in these amounts, such as other structures, personal property and loss of use, which are typically listed as coverage B, C and D, respectively, in coverage policies. And depending on your location, you may also need separate deductibles for wind or storm damage, will likely be determined based on a percentage of your dwelling coverage.

"While inflation has slowed down since its peak in June 2022, insurance rates are reactionary," Bankrate said in its September report. "The cost of home insurance is still increasing due to the impact inflation has had on the previous losses experienced by the insurance company, the elevated cost of building materials and the high likelihood of future extreme weather-related losses."

Home location matters for insurance costs

Across the U.S., people are dealing with risk of earthquakes, tornadoes, floods, hurricanes, wildfires and severe storms across the seasons. In California, which, as of Sept. 17, is battling six active wildfires, the growing risk of such events has left some areas "essentially 'uninsurable'," according to researchers at First Street Foundation, a nonprofit that studies climate risks. The group found that about 35.6 million properties — a quarter of all U.S. real estate — are facing higher insurance costs and lower coverage because of climate risks.

That combination also devalues their properties.

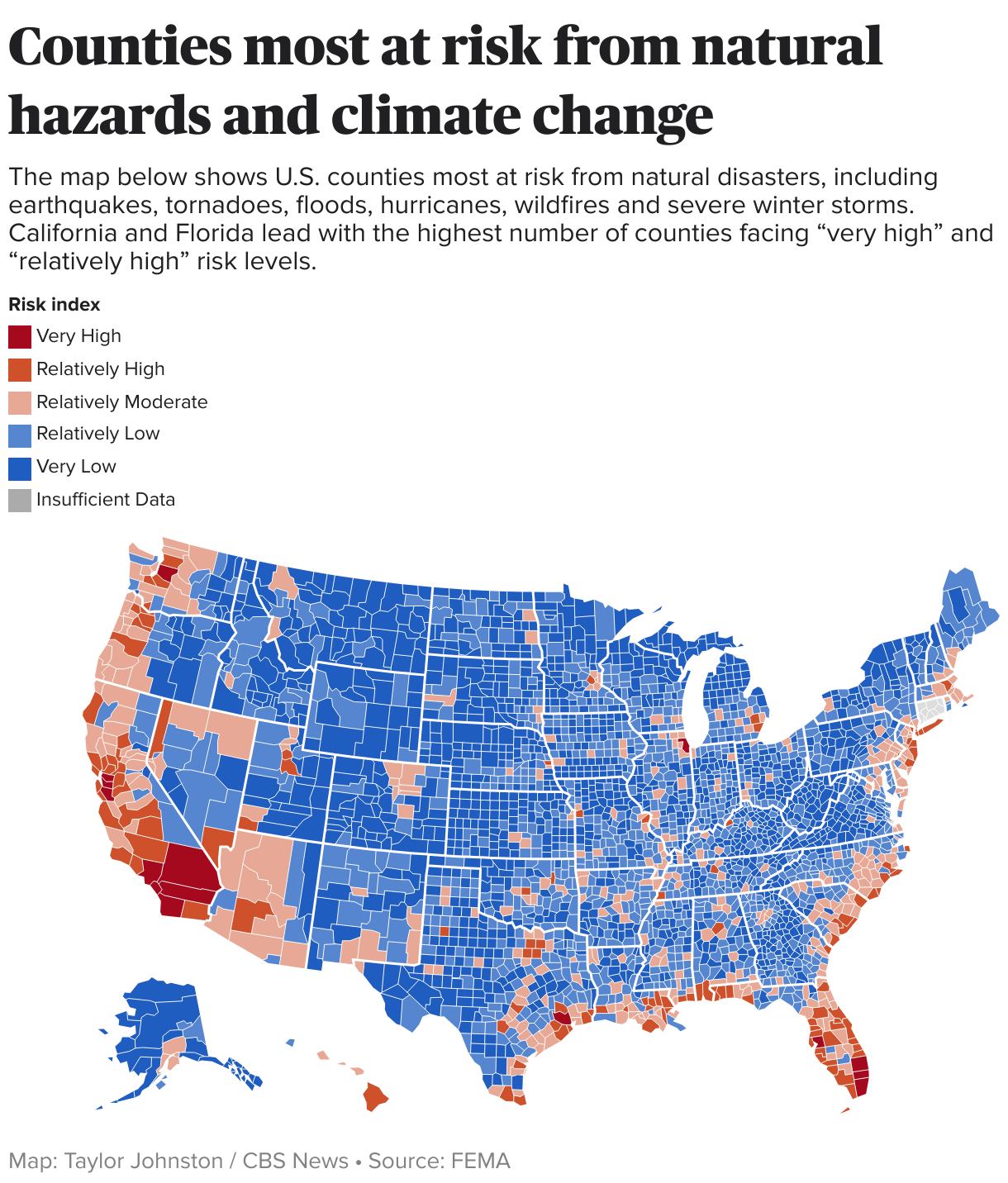

San Bernardino County, which accounts for six out of the 10 worst ZIP codes in the state for insurance non-renewals, is also among the most at-risk of natural hazards and climate change, according to FEMA. The county in Southern California is currently combatting both the Bridge and Line Fires, which combined have burned more than 93,000 acres.

The fire risk in California — which has also been battling the historically large Park Fire for nearly two months — is now so high that both Allstate and State Farm have paused sales of property and casualty coverage to new customers in the state.

"The cost to insure new home customers in California is far higher than the price they would pay for policies due to wildfires, higher costs for repairing homes, and higher reinsurance premiums," Allstate told CBS News.

AAA is also opting out of renewing some policies in Florida, a state that has seen increasingly devastating impacts of flooding and hurricanes. Without private insurance offers, it's up to insurance policies made available by the government, such as the National Flood Insurance Program, to assist.

It's not just an issue for coastal areas and wildfire-prone states. In fact, the most impactful weather events are those that do not get categorized with names.

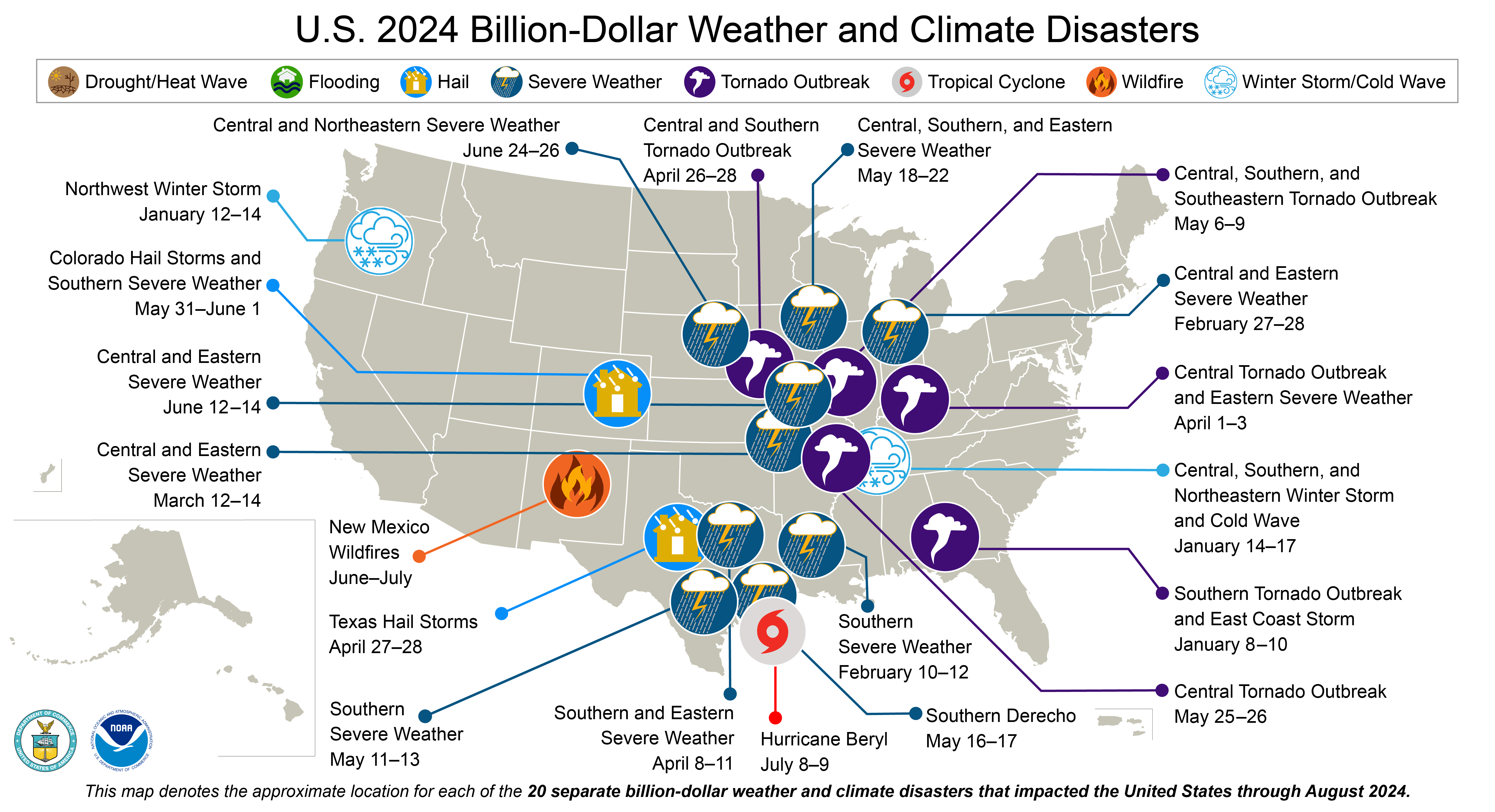

The Insurance Information Institute found in a May 2020 report that severe convective storms — thunderstorms — "are the most common and damaging natural catastrophes in the United States." Tornadoes are often a product of those storms, and Nebraska, the most expensive home insurance state on average, was impacted by five of the top 10 costliest U.S. catastrophes involving tornadoes, according to the report.

There have already been 20 billion-dollar disasters nationwide so far this year, as of Sept. 10, with 14 of those involving severe weather or tornadoes.

As the risk grows, affordability dwindles

Nearly half of U.S. homes face a severe threat of climate change, with about $22 trillion in residential properties at risk of "severe or extreme damage" from flooding, high winds, wildfires, extreme heat or poor air quality, according to a study earlier this year by Realtor.com.

But Bankrate has also found that more than a quarter of homeowners say they aren't financially prepared to handle the costs that come with it.

And it's not just homeowners. While last year was not the worst year for overall U.S. insured losses due to extreme weather, it was the worst year since at least 2014 for losses due to severe storms ($59.2 billion), according to data by AON.

Renters are feeling those impacts as well.

Between 2020 and 2023, multifamily housing development insurance rates increased by an average of 12.5% annually, according to a June report by the Bipartisan Policy Center.

"One affordable housing provider, National Church Residences, saw its property insurance premiums increase by over 400% in the six years leading up to 2023, along with higher deductibles and reduced coverage," the report says. National Church Residences provides affordable housing and independent and assisted living to seniors.

Last fall, NDP Analytics surveyed 418 housing providers across the U.S. who operate a combined 2.7 million units, including 1.7 million affordable housing units. They found that nearly a third of them saw premium increases of 25% or more from 2022 to 2023. To handle those costs, over 93% of respondents said they'd have to increase their deductibles, decrease operating expenses and/or increase rent. More than half said they would need to limit or delay investments in housing stock and projects.

How to lower home insurance costs

The driver behind extreme weather events — rising global temperatures largely fueled by the burning of fossil fuels — is not going away anytime soon. The continued release of greenhouse gases that trap heat within the atmosphere will continue to heat up the planet for thousands of years to come, even if overuse of those gases stopped today, which means that there are still decades to come of worsening climate disasters putting lives and homes at risk.

But home insurance is a game of measuring risk, and there are things you can do to better protect your home that could help lessen the blow of future weather disasters.

According to Massachusetts insurance agency C&S Insurance, resilient home features can make an impact on premium pricing. Storm shutters, reinforced roofing and flood barriers can all help lower the risk of damage to your house, and therefore, your wallet.

NerdWallet says that elevating your home's water heaters and electrical panels, developing wildfire-resilient landscaping and installing fortified roofing are among the things homeowners can do to reduce the impacts of flooding, fires and wind, respectively.

The Council on Foreign Relations, an independent nonpartisan organization, says that more government regulations on where and how homes can be built can also help reduce costs. The group says that stopping taxpayer dollars for buildings in high-risk areas and more investment in natural infrastructure, such as wetlands and trees, can also help reduce impacts from storm surges and heat.