Is the U.S. recovery too old for its own good?

The U.S. economic rebound has lasted 77 months so far. By historical standards, it's now a senior citizen. But does that mean a fresh recession is around the corner?

Not necessarily. Still, it's hard not a feel a little worried.

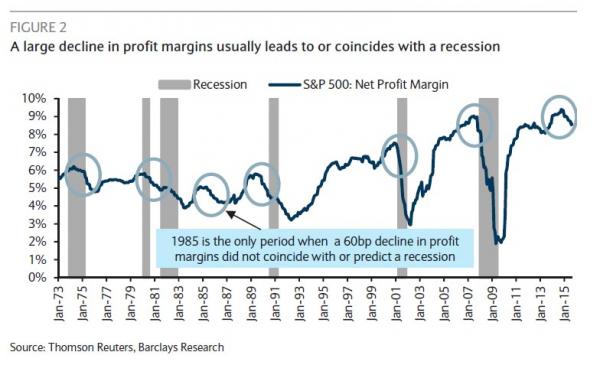

According to Yardeni Research, the average length of the country's previous 11 expansions was 58 months. In the past, corporate profit margins would start declining during the late stage of the expansion as poor investments accumulated, making the economic and financial markets vulnerable to the eventual tightening of Federal Reserve policy that has traditionally triggered recessions.

The chart below from Deutsche Bank shows how profit margins have started to roll over. When profit margins fall by 0.60 percent, as they already have in this cycle, it has marked the start of a recession in five of the last six occurrences. The lone exception was in 1985, which, like now, featured a large decline in crude oil prices.

FactSet data shows that with 463 S&P 500 companies reporting third-quarter results so far, overall earnings are on track to decline 1.8 percent from last year, marking the first back-to-back decline in quarterly earnings since 2009. Revenues are heading for their third consecutive quarterly decline.

A combination of a stronger dollar, weak commodity prices and a rise in inflation-adjusted wages along with a tightening labor market are all to blame for the decline in profitability. And that decline is resulting in a number of worrisome trends.

Industrial capacity utilization has stagnated. Capital spending has stalled. Semiconductor billings -- with chips used in everything from smartphones to refrigerators -- have dipped into negative territory on a year-over-year basis for the first time since 2013, according to World Semiconductor Trade Statistics.

Yet the team at Oxford Economics, while acknowledging the rare longevity of this recovery, believe it's not yet in a late-cycle phase and "has further room to expand." They base this on an analysis of five coincident and nine leading economic indicators that act like weather vanes to help determine where things stand.

Out of that group, only initial weekly jobless claims are flashing a late-cycle warning (how much longer can they stay as low as they are now?).

Manufacturing hours, the Fed's Senior Loan Officer Survey, corporate debt outstanding and the stock market's performance are suggesting caution is warranted.

But the economy's performance vs. its full potential (known as the output gap), payrolls, personal income, manufacturing and trade sales, housing permits, the relationship between short- and long-term interest rates and two different measures of credit market risk all continue to suggest the recovery remains in the middle of its cycle.

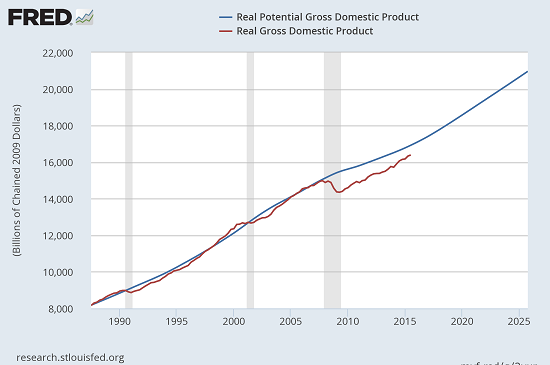

The Oxford team adds that old age alone isn't enough to kill a recovery. Recessions have historically happened due to economic overheating and the Fed's response to that. The chart above compares the current inflation-adjusted size of the economy (red line) to the Fed's estimate of its full potential output (blue line). Oxford believes that until the two lines converge, the recovery will tread on.

That said, the rebound could look much different in the years to come. It could be less about big business profits and stock market gains and more about long-delayed higher wages and rising labor costs -- that is, better take-home pay for regular Americans.