Facebook numbers won't worry investors, but should

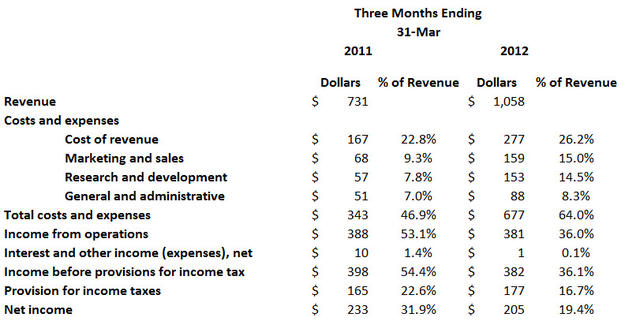

(MoneyWatch) COMMENTARY Facebook announced its 2012 Q1 earnings through an SEC filing. The long and the short of it: revenue up and profits down, both as a percentage and an absolute number. Revenue was up 45 percent year over year, from $731 million to $1.058 billion. Net income (profit) went from $233 million in 2011 to $205 in 2012. However, revenue was down 6 percent from the previous quarter.

Does this mean that potential investors will snub the expected IPO next month? Hardly. The results are not a disaster, and too many big investors have a lot to gain from a successful public offering (and much to lose if it fell flat). However, Facebook's quarterly earnings indicate some troubling weaknesses in the company that, while not driving it into the red, could interfere with its future. Revenue growth may weaken even as the number of users increases. That could leave Facebook vulnerable to deep-pocketed competitors like Google (GOOG).

Facebook buys Instagram user loveFacebook: Don't give passwords to employers

Yelp's strong IPO augurs well for Facebook

There was a significant jump in expenses. Here's our version of Facebook's consolidated financial statements, with the addition of numbers as a percentage of revenue:

Although revenue increased by 45 percent year over year, expenses doubled over the same period. But is that really surprising? Not given the pressure that Facebook is under to continue its growth, even as it claims a significant portion of the total number of Internet users in the world as users. You'd expect R&D and marketing and sales expenses to jump.

General and administrative expenses (overhead) grew rapidly, but still represent a small and manageable portion of revenue. When some companies -- Groupon (GRPN) comes to mind -- see a huge chunk of revenue going into this category, it is generally a sign to be concerned.

Reasons to be worried

Although investors badly want Facebook to succeed, there are signs that call for caution. For example, there's the question of users. The company claims more than 900 million active users per month. But here's the definition:

We define a monthly active user as a registered Facebook user who logged in and visited Facebook through our website or a mobile device, or took an action to share content or activity with his or her Facebook friends or connections via a third-party website that is integrated with Facebook, in the last 30 days as of the date of measurement.That is a slippery definition. For example, if you have a Facebook account and are tracked to a content site where you click the like button for something, that can be shared back to your account, even though you didn't log in and saw no ads.

Facebook said that its average revenue per user (ARPU) was $5.11 in 2011. Divide that into the $3.711 billion in revenue that the company shows for that year and you get an average number of users for the year of 726 million. The number of users is impressive, but the revenue per user? A fraction of what Google manages. It's ARPU that limits what the company can make.

Facebook says that worldwide ARPU last quarter was $1.21, up 6 percent over the previous year. But it was down 12 percent from the previous quarter. Facebook chalks it up to seasonality, which could be.

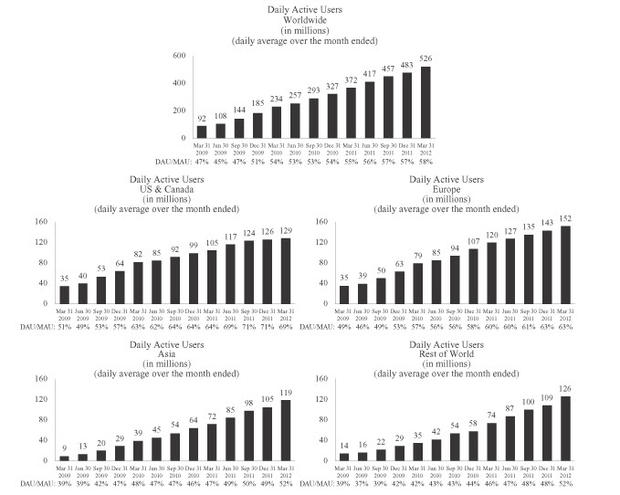

What if it wasn't? Half of the company's revenue came from North America during the quarter. That percentage has been declining as growth slows in this region while it expands elsewhere (as the graph below shows) in areas with "relatively lower ARPU." As things slow even more in North America and other parts of the world become a larger portion of growth and, eventually, total users, ARPU could well drop.

Not that the big investors in Facebook are worried. There will be enough positive activity that they will sell off shares, make a big profit, and leave any potential slowing to those who come in later.