Don't believe everything you read, this post excluded

(MoneyWatch) The paper "Performance and Persistence of Performance of Actively Managed U.S. Funds that Invest in International Equity", which appears in the summer edition of the Journal of Investing, is a rare type of read. Despite the overwhelming body of evidence that the large majority of actively managed funds underperform appropriate benchmarks and that the lack of persistent outperformance of the few winners makes it extremely difficult to identify the winners ahead of time, the paper makes claims to the contrary. Let's take a look to see if the author's findings hold up to scrutiny.

Using Morningstar's database, the paper studies the performance and persistence of performance of U.S. domiciled equity funds that invest in international equity for the 20-year period 1992-2011. The data comes from Morningstar Direct and contains 570 funds that invest more than 90 percent in equity. The author uses the annual Sharpe ratio to estimate risk-adjusted performance. Subsequently, the funds are separated into 13 region/style investment categories and shows that 9 of these categories exhibit a higher average Sharpe ratio than that of their respective benchmark. In addition, the report evaluates the existence of performance persistence by separating funds, at the beginning of every year, into quintiles according to their previous year performance for each one of the 13 investment categories. The author reached the conclusion that the results support the idea that there exists manager skill in the sample funds.

- This investment trend you want to follow

- George Costanza on investing, part 2

- Research shows bumpy road for active investors

Let's take a look at how the conclusions of the paper don't appear to be supported by the results.

1. The author claims that "performance is persistent." While making this statement he also finds "mixed results" regarding performance persistence. One of the findings was that investing in the loser quintiles actually outperforms investing in the winner quintiles in five of the 13 categories (about 40 percent), while following the opposite strategy allows for outperformance in the other eight. For example, for foreign small/mid-value stocks past losers beat past winners by a whopping 6.7 percent and did so with about 3 percent less volatility. For European stocks past losers earned twice the return of past winners with 4.4 percent less volatility. Similar results were found in the foreign large-growth stock category.

2. The author mentions that he used Morningstar's analyst's recommendations as to which style box to place a fund, and then compared performance to the appropriate benchmark. Because performance of actively managed funds can be driven by their exposures to asset classes and factors other than the chosen index benchmark, the proper way to do the analysis is to use a three-factor (beta, size, and value) or four-factor (adding momentum) model to determine if alpha (outperformance) was generated. The problem of "style drift" also creates issues with his use of the Sharpe ratio to compare performance across funds. The reason that the Sharpe ratio may not be a good measure to compare performance across funds is because standard deviation is an incomplete measure of risk and that there may be other risk factors -- the results may be driven by some funds having exposure to factors such as size, value and momentum that are different than that of the benchmark -- and style drift issues have proven to be important in studies such as this one.

3. It's well known that the Morningstar data suffers from survivorship bias. Yet, the author fails to discuss this issue. Further, the results directly conflict with prior research findings including the 2012 S&P Indices Versus Active scorecard (SPIVA) -- which does take into account survivorship bias -- which found that for the five-year period 74 percent of active international funds underperformed and 76 percent of active emerging markets funds underperformed.

4. There are also clear problems with statistical significance in the data. Approximately one-third of the 13 categories contain less than 10 funds for the 20-year period under analysis which implies that several of the within-category quintiles contain either 1 or 0 funds.

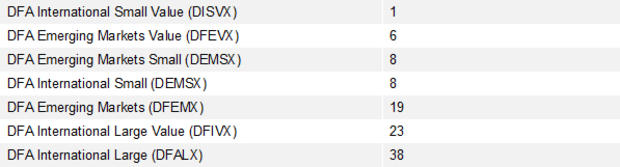

Additionally, to demonstrate that there are significant problems with the results, we can look at Morningstar's percentile rankings for the 15-year returns of various passively managed international funds run by Dimensional Fund Advisors (DFA), the largest provider of passive strategies that are not pure index funds. The table below shows the percentile rankings for the 15-year period ending July 30, 2013.

The passively managed funds of DFA outperformed the vast majority of active funds in every category. The average percentile ranking for the seven DFA funds is about 15. That means that of the active funds that managed to survive the full 15-year period, on average 85 percent underperformed passive strategies, even before considering the extra burden of taxes that active management typically imposes. What's also interesting is that the worst performance for active funds comes from the asset classes that are supposedly the least efficient -- small, small value and emerging markets!

We can also look at the relative performance of the three international index funds Vanguard runs. Their Total International Index Fund (VGSTX) has a percentile ranking of 29, their Emerging Markets Index Fund (VEIEX) has a percentile ranking of 36, and their European Index Fund has a ranking of 71. The active funds lost in two of the three categories with on average 55 percent underperforming their benchmark index. Again, keep in mind that there's survivorship bias in the data.

With the above knowledge, we'll let you draw your own conclusions as to whether or not the study's results are either theoretically or statistically supported.

Abhay Kaushik, "Performance and Persistence of Performance of Actively Managed U.S. Funds that Invest in International Equity," Journal of Investing, Summer 2013.

http://www.iijournals.com/doi/abs/10.3905/joi.2013.22.2.055

Image courtesy of Flickr user NS Newsflash.