Beware of junk-bond contagion

Even tough U.S. equities mostly moved higher on Monday in what was a harrowing, stomach-churning session, investors remain on edge heading into the first potential rate hike from the Federal Reserve in nearly a decade later this week.

Bond market weakness remains center stage as well, with issues in the high-yield corporate bond market now spreading to other credit areas, such as investment-grade bonds, setting the stage for more volatility in the days and weeks to come.

On Monday, the iShares Investment Grade Bond Fund (LQD) lost 0.7 percent to return to its early November lows. The iShares High Yield Bond (HYG) dropped another 0.9 percent as its 2013 lows are tested. And yet another high-yield credit fund -- the third in recent days -- ran into problems as Lucidus Capital liquidated its $900 million portfolio to return capital to investors.

Wall Street did its best to calm raw nerves, with analysts from Morgan Stanley noting that the high-yield bond market is a declining share of the overall bond market and that cash levels at high-yield mutual funds are at the highest level since 2012.

But the cavalcade of issues in play is hard to dismiss:

- The economic expansion is getting long in the tooth. At 78 months, it's already longer than 29 of the last 33 expansions since 1854.

- The drag from low energy prices, a stronger dollar and the expected rise in interest rates is set to push S&P 500 earnings down in this year's fourth quarter for the third consecutive quarter, something that hasn't happened since the financial crisis.

- The expected rise in interest rates, the vulnerability of high-cost U.S. shale oil producers and the drop in corporate profitability will likely push up bond default rates -- providing yet another reason for bond investors to sell into a thin market with light volumes. The lack of liquidity in some areas of the bond market as ultralow interest rates atrophied trading interest is the reason bond funds like Lucidus are running into trouble.

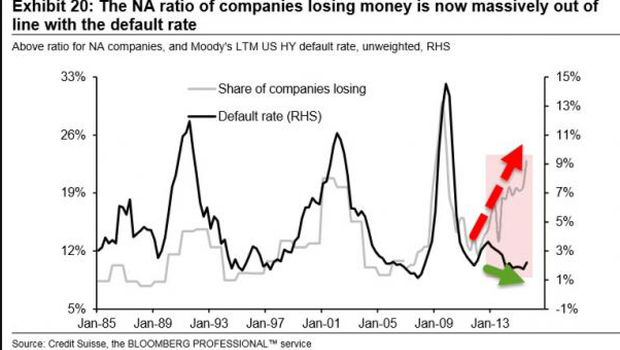

The chart above from Credit Suisse reveals just how serious the selling pressure in bonds could become, with the bond default rate diverging severely from the number of U.S. companies that are losing money outright. Bond prices simply aren't yet reflecting this new reality of lower profitability. Nor have they fully priced in a series of Fed rate hikes. The bond market is looking for fewer rate hikes in 2016 than Fed officials are.

All eyes are now turning to Wednesday's "hike/no hike" decision from the Fed. Expectations are for a 25-basis-point increase in the short-term federal funds policy rate -- up from near zero percent now. Focus will be on the central bank's updated summary of economic projections, including the "dot plot" of interest rate expectations, for clues about the pace of any subsequent rate hikes in 2016.

Chatter is growing that the Fed will soon have to start cutting rates again. More than half of the 65 economists surveyed by The Wall Street Journal see rates back near zero in the next five years. Ten expect them to fall into in negative territory. Their concern centers on two facts: No major central bank has been able to raise interest rates and keep them high since the financial crisis, and the Fed has never waited this long into the business cycle to start tightening monetary policy.

That makes the odds of a policy mistake very high.