Could a zombie mortgage put you at risk of foreclosure? Long-forgotten debt is coming back to haunt homeowners.

Jose Arzate once dreamed of a peaceful retirement in a quiet neighborhood in his hometown. A 24-year veteran of the county probation office, Arzate thought he had achieved the American Dream when he purchased a three-bedroom ranch house in Santa Maria, California, 20 years ago.

"As an immigrant, you have a dream, a dream of owning your own home. It's your castle. It's for your family," said Arzate.

The son of Mexican immigrants, Arzate envisioned the family home would be passed on for generations. But while he thought he was building a future for his family through equity in his home, a hidden financial nightmare was eating away at his dream.

"I woke up one morning to find sheriffs outside my door," Arzate said. "I had no idea this was coming. I was in bed, starting my day, and suddenly, I was being evicted."

What Arzate was dealing with was a zombie mortgage.

Arzate had modified his loan 13 years earlier, taking out a second mortgage to manage expenses. He assumed his monthly payments covered both mortgages. Unknown to him, he says, the second mortgage had been sold to a different servicer. Arzate said he never got a separate monthly statement for that second mortgage until it was too late.

"I didn't get a bill at all," he said.

More than a decade later, that unpaid loan was resurrected with interest and late fees, inflating the debt from $65,526 to $139,211.

Federal law mandates lenders send statements for home loans, but some don't comply. Arzate said he was told he needed to pay the lump sum or leave.

"If you owe money on a credit card, they send you a bill every month," Arzate said. "They didn't do that. They just evicted me."

The rise of zombie debt

Zombie debt refers to long-forgotten or old debts that resurface, often with accumulated interest and fees, threatening the financial stability of unsuspecting homeowners. These debts are frequently sold to new servicers who then aggressively pursue the outstanding amounts, sometimes leading to foreclosures.

"It's the mortgage you thought that was dead that has come back from the grave to come and haunt you," said Rich Szerman, a Realtor in California.

Szerman said he's seen similar cases among his clients.

"Most people get them because they filed a bankruptcy and they thought that discharged a junior lien, a second [mortgage], or they did a modification and they thought it was included. Or they sometimes get letters from their bank saying that your debt is discharged and is no longer collectible and no further payments are necessary," he said. "[And yet] the debt still exists even under those circumstances."

A ticking time bomb

After years of combat, Iraq War veteran Laverne Simmons found solace in her modest Inglewood, California, home. Yet, after more than a decade of timely mortgage payments, she was blindsided by a default notice.

"I haven't been late or asked for a payment arrangement or anything. So I was really confused," said Simmons.

While working to get her disability benefits situated with the Army, the medical bills for her wartime injuries piled up. Simmons took out a second mortgage in 2014 to help make ends meet.

Just like Arzate, she believed her monthly payment covered both mortgages. She said she never received statements for the second loan. Though some aspects of their claims, like the lack of billing, were impossible for CBS News to verify, they fit the pattern experts described.

Over time, with interest and fees, her $65,000 loan ballooned to over $140,000. Faced with foreclosure, she sought help from Rich Szerman.

"These debts get sold to vulture capitalists who enforce the full loan value with back interest and penalties," Szerman said. "If you don't pay, they take your house. It's unethical, immoral, and wrong."

Szerman is also working with Los Angeles single mother Teresa (who asked that her last name not be used).

"Back in 2009, I had to modify my [mortgage] loan," she said. "I was going through a divorce. I had 2-year-old twins."

Teresa says she never received a monthly statement for her new second mortgage, and assumed it rolled into her primary loan payment.

In January, she discovered she'd been mistaken, and learned her loan had been sold to a new servicer.

"I received a letter from Statebridge Company notifying me that I owed them over $180,000, with an initial payment due of over $50,000, and that I was behind by over 5,000 payments," she said. "I looked at this, and I, I mean, I didn't recognize it. I didn't know what it was from."

Teresa says Statebridge, a debt collector, has refused to negotiate her balance.

"It's beyond scary," she said. "To know that there might be a moment where we may have to move. And given the real estate prices and the rental prices in Southern California, I'm not looking at relocating to the house next door or to an apartment next door. I'm looking at — I can't afford to live in California anymore if I can't stay in my current home."

A spokesperson for Statebridge declined to comment on Teresa's case.

The legal and ethical battleground

Rohit Chopra of the federal Consumer Financial Protection Bureau said his agency has seen an increase in complaints about zombie mortgages, with some debt collectors skipping steps in the foreclosure process.

"Many times, we're hearing they're targeting older homeowners, people who may be sitting on a lot of home equity," Chopra said. "A lot of this is totally under the radar, and much of these practices are illegal."

Chopra said they don't have data on how widespread the problem is, but he encourages homeowners facing zombie debt collection to immediately report it to the CFPB.

"This is a big failure from the lead-up to the financial crisis where regulators in Washington weren't watching what was happening on the ground in local communities," he said. "We have been reaching out across the country to ask, where is this happening and what can we do about it?"

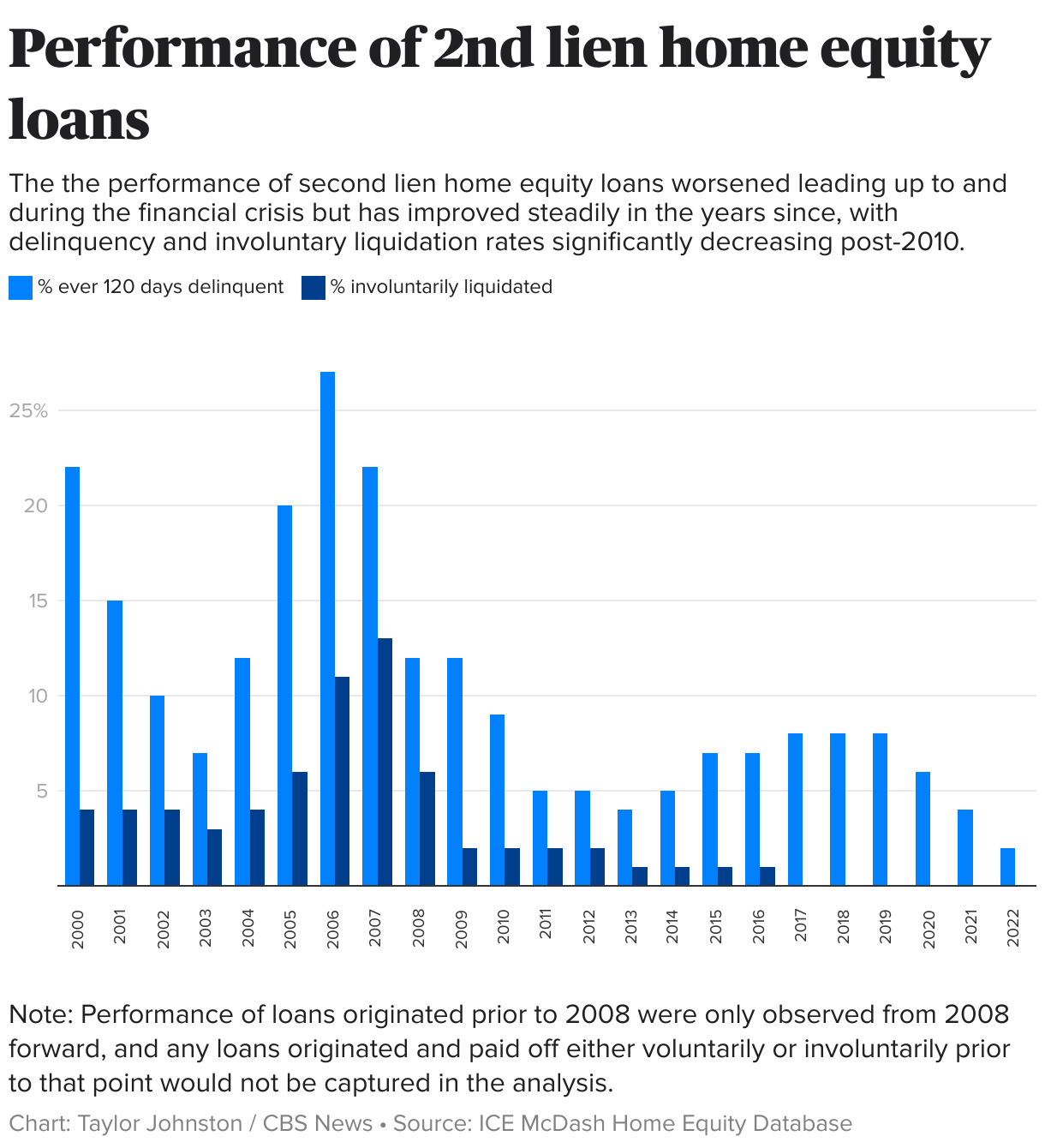

Intercontinental Exchange Inc., or ICE, has been tracking performance on home equity loans since mid-2008, based on a subset of the market. The data reflects the impact of the financial crisis, showing high delinquency and liquidation rates around 2006 through 2008.

The ICE database tracks two key metrics: the percentage of loans ever 120 days past due and the percentage of loans involuntarily liquidated. The liquidations, reported by servicing companies, include events like foreclosures, the lender writing off the debt as a loss, or the lender selling the property for less than what's owed.

The data shows that delinquent and liquidated second mortgages spiked, impacting more than 30% of all second mortgages in 2006 and 2007. It is from that era that many old mortgages are being resurrected.

Simmons said she believes the debt holder on her second mortgage, Real Time Resolutions, waited until economic development in her neighborhood began increasing property values to send her notice.

"They just laid dormant until there was a time that I had enough equity, and then things started building over here, like the SoFi [Stadium], the Clippers [arena], and then that's when," she believes, "they were ready to strike, like a snake, just waiting for the right moment."

Real Time Resolutions recently settled a class action lawsuit with a different homeowner who claimed she'd been foreclosed upon without ever receiving the required monthly statements. The company denied wrongdoing but told CBS News they weren't "interested" in commenting.

Protecting yourself

Zombie debt isn't confined to mortgages. It can encompass medical bills, student loans, and even auto loans, lying dormant until a new servicer revives them.

To avoid falling victim to zombie debt, CFPB urges consumers to regularly check their credit reports for any liens or unfamiliar debts. If a suspicious bill appears, it's crucial not to pay it immediately. Instead, contact an attorney or local legal aid group to navigate the complexities of these claims.

"Don't pay a bill that is for something you don't owe," said Chopra. "File a complaint with the CFPB and talk to someone you trust who can help you navigate this process."

Fighting back

Both Arzate and Simmons are determined to fight back.

"I served my country, got injured, and now I have to go through this," Simmons said. "It's been pure hell. But I'm determined to fight for my home."

While Arzate's home was auctioned, he is suing to reclaim it while still making monthly mortgage payments. Meanwhile, he lives with his adult son in a crowded home, his wife staying with family to save money.

"Twenty years of memories are gone, but we're going to get it back," Arzate said.