Trouble brews in the bond market

Market bubbles -- those victories of red-hot emotion and greed over reasoned emotion -- have focused on many different things throughout history. Fancy tulip bulbs. Shares of Pets.com. Miami condos.

But the common thread that pops these bubbles is this: When the deviation from fair value gets too large. When risk is no longer properly rewarded. Or more simply, when these things just get too expensive.

This could be happening in the corporate bond market right now.

Consider that, as a consequence of low oil prices, Exxon (XOM) has lost its top "AAA" credit rating from Standard & Poor's after more than six decades -- leaving Johnson & Johnson (JNJ) and Microsoft (MSFT) as the last two remaining U.S. corporations with that golden triple A.

Yet that hasn't stopped investors from devouring its debt: Exxon sold a record $12 billion in bonds earlier this year, with Bloomberg quoting Andrew Brenner, head of international fixed income at National Alliance Capital Markets in New York, saying the pressure on its credit rating wasn't really weighing on XOM's borrowing costs.

This reflects a broader trend.

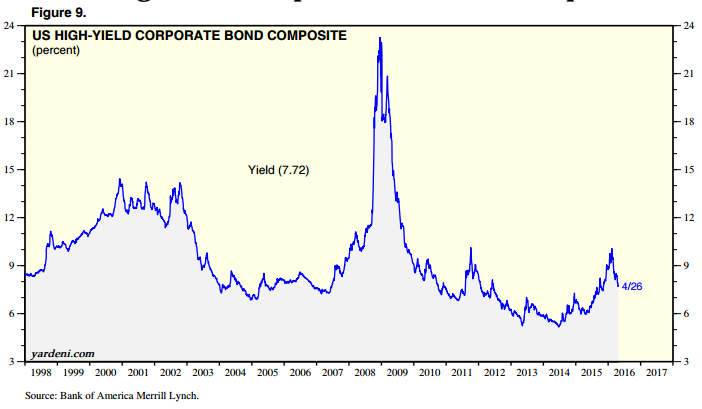

Through the end of March, year-to-date corporate defaults had jumped to the highest level since 2009, led by a failure of weak, high-cost energy companies in this difficult environment (chart above). Defaults of high-yield, or junk, bonds totaled $14 billion through the first two weeks of April alone -- the highest monthly volume in two years, according to Fitch.

Overall, 2016's first quarter marked the fifth-highest quarterly default total on record at $31.4 billion, according to JPMorgan. The only four larger quarters in terms of default volume were $76.6 billion in first-quarter 2009, $55 billion in second-quarter 2009, $40.2 billion in second-quarter 2014 and $37.9 billion in fourth-quarter 2009.

More is coming, said Bank of America Merrill Lynch's high-yield strategist Michael Contopoulos, as "cumulative losses over the length of the entire [default] cycle could be worse than we've ever seen before." His reasoning is based on tepid estimates for U.S. GDP growth as well as headwinds on corporate earnings and cash flow.

Earlier this month, JPMorgan's economists were looking at GDP expanding at just 0.6 percent for the first quarter and 2 percent for the second quarter. And Contopoulos noted that six out of 17 sectors realized negative year-over-year adjusted operating income in fourth-quarter 2015, with nine sectors in the red on an unadjusted basis (removing "one-off" charges, etc.).

According to FactSet data, through April 22 with 26 percent of S&P 500 companies reporting, first-quarter earnings are set to decline 8.9 percent for the worst result since 2009 and marking the fourth consecutive quarterly decline in profitability.

Contopoulos' main concern is that aggressive intervention by the major central banks -- from negative interest rates in Japan to very slow rate hikes by the Federal Reserve and corporate bond purchases by the European Central Bank -- is prolonging the inevitable reconciliation of faltering fundamentals with bond pricing.

"But the very same policies which helped alleviate the pain [of the last recession] will likely add to the severity of the next one," he said. "This is because many of the companies that should have defaulted seven years ago but instead received a lifeline will likely shutter doors now."

Why? Because operating earnings have not kept up with the growth of debt during this expansion. The final nail will be an increase in interest rates, which will hike financing expenses and force weak companies into insolvency.

That hasn't happened yet because investors -- instilled with confidence by the central banks -- have yet to price this reality into the market. The chart above shows how bond yields have actually collapsed since February as the market rebounded out of the mid-month low. The question is: Will the turnaround prove a false dawn as in early 2008, or the start of a prolonged turnaround a la 2011?