Dodd-Frank law's legacy: safer banks, banker headaches

Is the Dodd-Frank financial reform law a boon or a bane? President Donald Trump is going for bane, and on Friday moved to dismantle much of the regulatory apparatus that the 2010 law created.

“Today we are signing core principles for regulating the United States financial system,” Mr.Trump said as he issued an executive order that directs regulators to make a plan for scaling back Dodd-Frank, with the aim of freeing banks to lend more to businesses. He previously has called the act “a disaster.”

Mr. Trump also wants to rein in the Consumer Financial Protection Board, which Dodd-Frank hatched. The CFPB oversees financial products like mortgages and credit cards, and has become a major irritant to the banking industry. Plus, the president on Friday also signed a separate order that imposes a six-month delay on an Obama administration rule that tightens rules on retirement advisers.

A close review of the financial industry, however, finds that Dodd-Frank has made banks safer, although saddling them with questionable costs and regulatory headaches. Whether the law actually hindered lending is up for debate, because loans have recovered since the Great Recession -- although opponents say lending would have been stronger without the law’s impediments.

The 2010 law, authored by two Democratic lawmakers, Rep. Barney Frank of Massachusetts and Sen. Christopher Dodd of Connecticut, was in response to the 2008-09 global financial crisis. Many U.S. banks teetered on the edge of collapse and required federal bailouts. But both Dodd and Frank are now retired from Congress -- and the banking industry wants to retire their law, or at least soften it, under President Trump.

Wall Street is well represented within the new administration, with a large number of top officials hailing from Goldman Sachs (GS), arguably the banking industry’s most powerful player. Steven Mnuchin, a former Goldman partner, is the Treasury secretary designate; Gary Cohn, the firm’s previous second-in-command, is chairman of Mr. Trump’s Council of Economic Advisers; and Stephen Bannon, once a Goldman banker, is the president’s top strategist.

Until Mr. Trump’s election, large banks’ stock prices had weakened as investors doubted they could improve profits enough amid a strict regulatory climate. Since his election, U.S. bank stocks as a group are up a whopping 25 percent, compared with a gain of about 7 percent for the broader S&P 500 stock index.

Let’s review what the law has produced:

Safer banks. Dodd-Frank pushed the banks to boost their equity capital and lower their debt levels. Fresh in their minds was what happened to Lehman Brothers, whose 2008 disintegration touched off the financial crisis. Lehman, seeking to beef up its then-bounteous returns from mortgage-backed securities, had a debt-to-equity ratio of as much as 60 to 1. When mortgage bonds sank, so did Lehman.

The Federal Deposit Insurance Corporation likes to see banks maintain a debt-to-equity ratio of about 10 to 1. This means that, for every dollar of equity, the bank has $10 of debt. That larger equity cushion allows an institution to better withstand losses from economic downturns.

Lehman was not an FDIC-covered bank, and Bush administration officials said at the time they lacked the authority to save it. Under bailout legislation and Dodd-Frank, that changed. Now, the government has a lot more power over them. Major financial organizations, whether traditional commercial banks like JPMorgan Chase (JPM) or investment firms such as Goldman Sachs, must take annual stress tests to measure how well they can weather a storm.

“Now they can withstand two financial crises,” said Mike Mayo, a banking analyst with brokerage firm CLSA. These days, the ratios across the board are more in line with the FDIC’s desired level.

Of course, the banks are now certified members of the too-big-to-fail club. Critics suspect that, should all the new bulwarks fall, Washington once again will need to rescue them at great expense.

Bank profitability: a mixed picture. In raw dollars, banks are hardly suffering. According to the FDIC, their net income hit an all-time high in 2016’s third quarter. Meanwhile, the amount of unprofitable banks dipped to its lowest level since 1997.

In addition, nothing has stopped the larger lenders from ladling out generous dividends to investors. The average bank dividend is 2.4 percent, higher than the S&P 500’s 2.1 percent. Plus, the amount of earnings that goes to dividends averages almost a third.

With a trend toward rising interest rates, driven by the Federal Reserve’s hiking of its benchmark rate, lenders’ earnings should grow nicely. Banks make money off the difference between what they receive in loan interest and the lower cost of paying depositors -- and escalating rates make that gap widen, to the lenders’ delight.

That said, the picture could be better, and critics say Dodd-Frank has held back banks from performing to their full potential. Indeed, banks’ average return on equity, a measure of profitability, has dropped to 9 percent from its pre-recession high of 15.5 percent. Of course, it fell to minus 1 percent in 2009.

Complying with regulations is expensive, and eats into earnings. CLSA’s Mayo said the cost of regulation has added $100 billion to banks over the next five years. A study by research firm Federal Financial Analytics found that the six largest U.S. banks shelled out some $70 billion for regulatory compliance from 2008 through 2013.

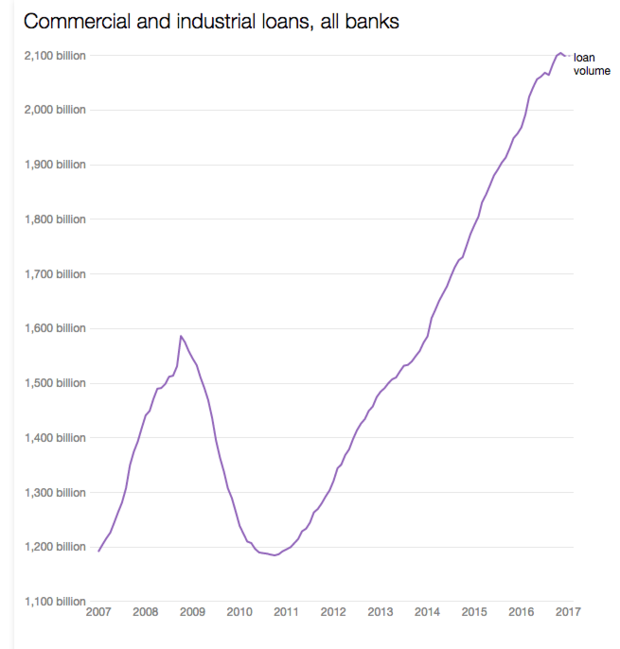

Lending is turning up. Despite criticism that Dodd-Frank has hindered lending, the volume of it has expanded steadily since the aftermath of the recession. In December, St. Louis Federal Reserve figures show, commercial banks lent more than $2 trillion, almost double the level from December 2010, its low point.

The fact that banks have paid out nice dividends calls stories of their loan pullbacks into doubt, said Anat Admati, a Stanford University economist who specializes in finance and financial markets. “Don’t believe their B.S.,” she said. “Banks have plenty of money.”

After the recession, banks did tighten lending standards, especially for home mortgages -- the root of the crisis. But lately, they have eased the guidelines and more mortgages are gaining approval.

Community banks bear biggest impact. Smaller lenders are where many Americans still get their mortgages and business loans, despite large banks commanding much of the nation’s bank deposits and loan volumes.

Certainly, small community banks have suffered inordinately in the wake of the financial crisis because they have fewer resources than the major lenders, and regulatory burdens hit them hardest. Community banks pay out some $4.5 billion in annual costs, according to a 2015 study by the St. Louis Federal Reserve

Camden Fine, head of the Independent Community Bankers of America, welcomed Mr. Trump’s move. “Onerous regulatory burdens on community banks are stifling lending and innovation in local communities, hindering economic and job growth across the nation,” he said.

Should Mr. Trump get his way, that complaint likely will be increasingly rare in the banking community.